December was a good month for stock and bond markets, capping off an odd and volatile year. When looking at the performance for the year overall, it turned out to be an average year despite the sharp drop and panic in March.

December 2020 Market Performance

All index returns are total return (includes reinvestment of dividends) and are in Canadian Dollars unless noted.

| Other Market Data | Month-end Value | Return for December 2020 | 2020 YTD return |

|---|---|---|---|

| Oil Price (USD) | $48.52 | +7.01% | -20.54% |

| Gold Price (USD) | $1,895.10 | +6.41% | +24.42% |

| US 3 month T-bill | +0.09% | +0.01%* | -1.46%* |

| US 10 year Bond | +0.93% | +0.09%* | -0.99%* |

| USD/CAD FX rate | 1.2732 | -1.80% | -1.97% |

| EUR/CAD FX rate | 1.5608 | +0.64% | +7.03% |

| CBOE Volatility Index (VIX) | 22.75 | +10.60% | +65.09% |

*Absolute change in yield, not the return from holding the security.

December was a good month for stock and bond markets, capping off an odd and volatile year. When looking at the performance for the year overall, it turned out to be an average year despite the sharp drop and panic in March.

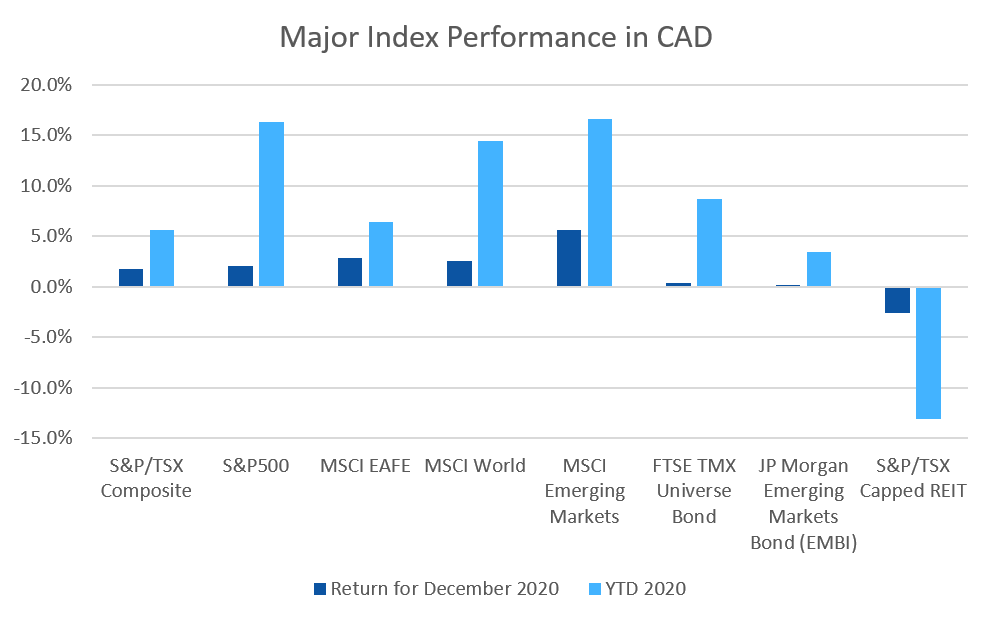

The S&P/TSX Composite was up +1.4% for December, finishing the year up +2.2%. The TSX was positive in 8 of 12 months, which is actually a little above the average for the previous 25 years. The S&P/TSX Small Cap Index was up +5.5% for the month and +10.0% for the year. In the US, the large cap S&P500 was up +3.8% for the month and +18.4% for 2020, while the small cap Russell 2000 index was up +8.5% for the month and +18.4% for 2020.

EAFE (Europe, Australasia & Far East) stocks were up +2.4%, but it wasn’t enough to turn the index positive for 2020, and it finished at -1.4%. European and British stocks were both up for December, +2.1% and +3.1%, respectively, but both were unable to turn positive for 2020, completing the year at -4.3% and -14.3%. Japanese stocks were up +3.8% for the month and +16.0%. Emerging market stocks were among the best performers for December and 2020 at +5.9% and +16.6%, respectively.

Bonds were largely positive in December. The major Canadian bond index, the FTSE/TMX Universe Bond Index, was up +0.4% and the FTSE/TMX Short-term Bond Index was up +0.2%. Those indices finished 2020 up +8.7% and +5.3%. As in November, both US investment grade and high yield/distressed bonds were positive for the month. Investment grade was +12.2% for 2020, while high yield was up about half that. Emerging market bonds were up +0.2% for the month and +3.4% for 2020.

Oil was up +7.0% in December and finished 2020 down -20.5%. Gold was up +6.4%, finishing the year +24.4%. The diversified Bloomberg Commodities Index was up +5.0% for December, which wasn’t enough to salvage the year, and it finished down -3.5%.

The Canadian Dollar (CAD) gained +1.8% against the US Dollar in December, and +2.0% over the year. Against the Euro, CAD lost -0.6% in December and -7.0% for 2020.

December 2020 Economic Indicator Recap

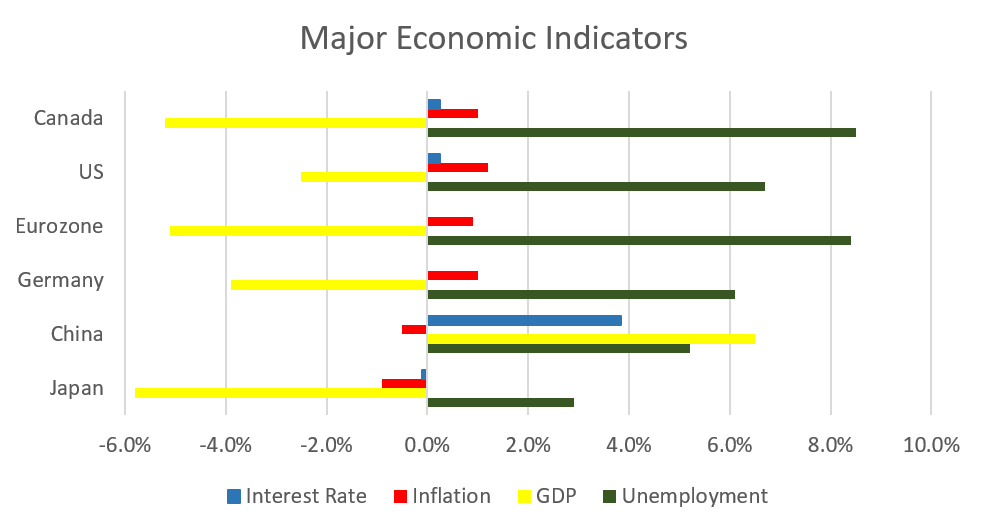

Below are the readings received in December for the major economic indicators: central bank interest rates, inflation, GDP and unemployment.

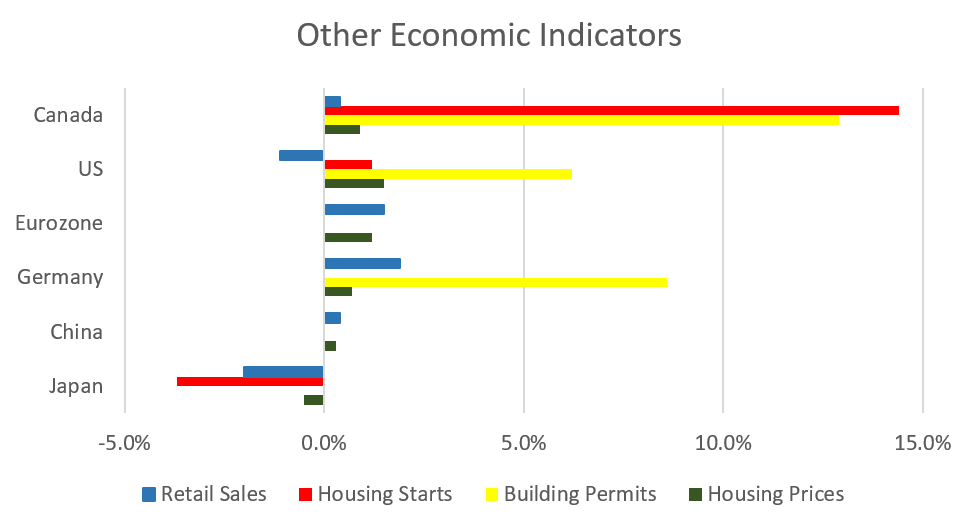

Below are the current readings on a few other often followed economic indicators: retail sales and housing market metrics.

A Closer Look at the Canadian Economy

Canada’s unemployment rate declined slightly to 8.5% in November. The economy added 62,000 jobs during the month, 99,000 of which were full time jobs offsetting the loss of 37,000 part-time jobs. Youth unemployment declined to 17.4% the lowest rate since March.

Housing prices across Canada were up +0.9% in November, the strongest gain for the month of November in the 22 years of the index. Hamilton was the top performer at +1.9%, followed by Halifax (+1.6%), Montreal (+1.4%) and Ottawa (+1.3%). For the third consecutive month, mone of the major Canadian housing markets were down.

The level of new housing starts rose +14.4% in November to 246,000 units. Urban construction rose +15%, as multifamily construction rose +22.5%. Building permits rose +12.9% in November to $9.4 billion, the third highest on record, led by large permits for multifamily constructions in BC and Ontario.

The inflation rate for November was +0.1%, and +1.0% on an annual basis, the highest since February. Core inflation which excludes more variable items such as gasoline, natural gas, fruit & vegetables and mortgage interest was +1.5%. The cost of food, shelter, and recreation, clothing & footwear rose.

Retail sales were up +0.4% in October, the sixth month of positive growth. Sales rose at car dealers, sporting goods stores, and furniture stores. Compared to a year ago retail sales were up +7.5%.

Canada’s GDP was up +0.4% in October, the sixth consecutive monthly gain, but economic activity remains 4% below pre-pandemic levels. Both the goods and services sectors were positive; 16 of 20 industrial sectors posted gains.

As expected, the Bank of Canada left its benchmark interest rate at 0.25% at the December 9 meeting. The BoC has adjusted its quantitative easing program towards purchasing longer-term bonds with total purchases of at least 4 billion per week. Policy makers noted that the economic recovery will continue to require extraordinary measures until into 2023.

*Sources: MSCI, FTSE, Morningstar Direct, Trading Economics