October was a good month for most equity markets, while fixed income and emerging markets were down. REITs had a fantastic month and are on track for their best year in decades.

October 2021 Market Performance

All index returns are total return (includes reinvestment of dividends) and are in Canadian Dollars unless noted.

| Other Market Data | Month-end Value | Return for October 2021 | 2021 YTD Return |

|---|---|---|---|

| Oil Price (USD) | $83.57 | +11.03% | +72.24% |

| Gold Price (USD) | $1,783.90 | +1.73% | -5.87% |

| US 3 month T-bill | +0.05% | 0.01%* | -0.04%* |

| US 10 year Bond | +1.55% | +0.03%* | +0.62%* |

| USD/CAD FX rate | 1.2384 | -2.80% | -2.73% |

| EUR/CAD FX rate | 1.4338 | -3.13% | -8.14% |

| CBOE Volatility Index (VIX) | 16.26 | -29.73% | -28.53% |

*Absolute change in yield, not the return from holding the security.

October was a good month for most equity markets around the world, and a down month for most fixed income markets as the possibility of rising interest rates came to the forefront.

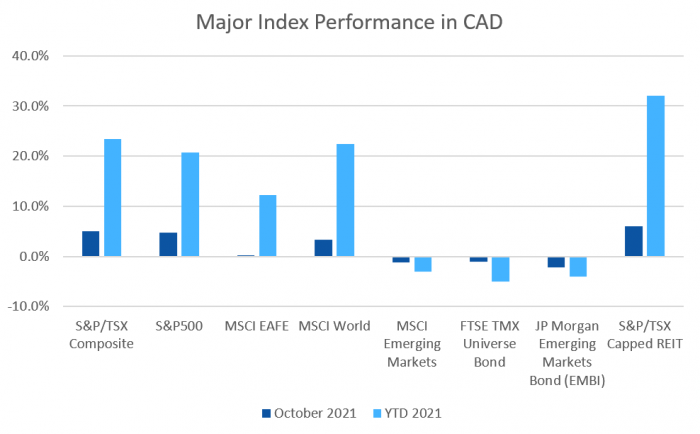

The S&P/TSX Composite was up +5.0% for October, its best month of 2021 and the best month since the sharp drawdown seen at the start of the pandemic. The S&P/TSX Small Cap performed similarly, gaining +5.1% in October. In the US, the large cap S&P500 gained +7.0%, its best month of the last twelve. The index of US small cap stocks, the Russell 2000, gained +4.2% for October. The tech focused Nasdaq also performed well, gaining +7.3% for the month. All of the indexes mentioned above (except Russell 2000) are up more than 20% for 2021.

Non-North American equities continue to lag. The broad index of EAFE (Europe, Australasia & Far East) stocks gained +2.1%, in October. European stocks alone performed better, gaining +3.6%. Japanese stocks were one of the losers in October, declining -1.9%; they’re up only +5.3% for 2021. Emerging market stocks were up +0.8%, and are essentially flat for 2021 (-0.2%).

Bonds were mostly down in October. The major Canadian bond index, the FTSE/TMX Universe Bond Index, lost -1.1% in October as did the FTSE/TMX Short-term Bond Index. Both are negative for 2021; -5.0% for the Universe index and -1.5% for the Short-term index. US investment grade bonds were one of the few positives in the global bond markets in October. ICE BoA AAA index gained +0.9%, but it’s still down -2.5% for 2021. The BBB index gained +0.2% for the month, and is now flat for 2021. High yield had it’s first negative month in over a year, the HY Master II Index was down -0.2%, and -0.4% for the CCC and lower (the real junky stuff) Index. Emerging market bonds were down -2.1%, bringing the YTD loss to -4.1%. Unless EM bonds have spectacular performance in November and/or December, they will post their first negative year since 2007(!).

REITs rebounded strongly in October, gaining +6.0%, bringing their YTD performance to +32.1%. Unless the wheels fall off, 2021 will be the best year for REITs since 2009, when they gained +55.2% following the historic losses seen during the 2008 financial crisis.

Oil gained +11.0% in October, breaking through the US$80 a barrel level for the first time since the summer of 2014. Oil is up +72.2% in 2021! Gold was up +1.7% for the month; its still down -5.9% for the year. The diversified Bloomberg Commodities Index had another good month, gaining +2.6% in October; its now up +32.4% YTD its best year since the start of our records for the index going back to 1994.

The Canadian Dollar (CAD) gained strength in October, welcome news for those hoping to travel as international borders start to reopen. Against the US Dollar CAD gained +2.8%, and +3.1% against the Euro.

October 2021 Economic Indicator Recap

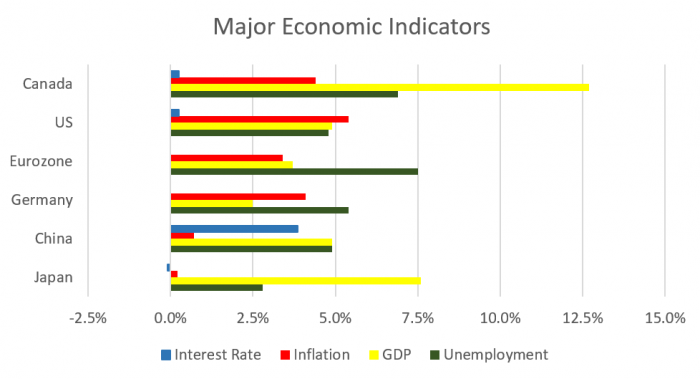

Below are the readings received in October for the major economic indicators: central bank interest rates, inflation, GDP and unemployment.

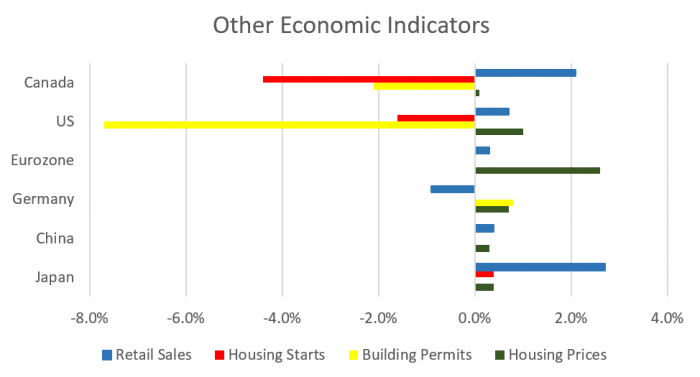

Below are the current readings on a few other often followed economic indicators: retail sales and housing market metrics.

A Closer Look at the Canadian Economy

Canada’s unemployment rate declined for the fourth consecutive month, dropping to 6.9% in September, the lowest rate since the COVID-19 pandemic began in early 2020, as most provinces implemented vaccine mandates allowing more non-essential venues to reopen. The economy gained 157,100 jobs; 193,600 new jobs were created while 36,500 part time jobs were lost. Total employment has now recovered to pre-pandemic levels.

Housing prices across Canada were basically flat in September, gaining only +0.1%. Gains were led by Winnipeg (+1.0%), followed by Victoria (+0.6%), and Toronto, Quebec City and Halifax all at +0.4%. Vancouver and Ottawa were the only markets that were down in September.

The level of new housing starts declined for the fourth month in a row, losing -4.4% in September to 255,000. Urban housing starts declined -4.5%, due to a decline of -4.0% in multi family construction. Single family home construction declined -5.9%. Building permits issued declined -2.1% in August to $9.7 billion, far below market expectations of a +3% increase. Declines in Ontario and BC more than offset the gains in all other provinces. Residential building permits declined -8.3%, driven by a -15.9% decline in multi-family building. Meanwhile, commercial building permits rose +14.9%.

The inflation rate for September was +0.2%, and +4.4% on an annual basis – the highest annual inflation rate since February 2003. Part of the reason for the higher level of inflation is the lower price levels seen in the midst of the worst of the pandemic last year, as well as ongoing supply chain issues. Prices rose in all eight components of the index. Core inflation which excludes more variable items such as gasoline, natural gas, fruit & vegetables and mortgage interest was +3.5%.

Retail sales were up +2.1% in August, with 9 of 11 sectors posting gains. Sales were up +8.4% compared to a year ago. Most of the gains came from supermarkets and grocery stores, as well as clothing stores and gasoline stations.

Canada’s GDP was up +0.4% in August. 15 of 20 industries saw growth, led by accommodation (+11.3%) and restaurants (+5.4%).

As expected, the Bank of Canada left its benchmark interest rate at +0.25% at the October 27th meeting. The benchmark interest rate is expected to remain at its current low level until into second half of 2022. The big headline is the BoC ended their quantitative easing program of purchasing government and corporate bonds, returning to the pre-pandemic policy of restricting purchases to reinvestment of maturing bonds.

*Sources: MSCI, FTSE, Morningstar Direct, Trading Economics