February was a strong month for equity markets, much stronger than usual for that month of the year. Fixed income on the other hand, was down almost across the board.

February 2021 Market Performance

All index returns are total return (includes reinvestment of dividends) and are in Canadian Dollars unless noted.

| Other Market Data | Month-end Value | Return for February 2021 | 2021 YTD return |

|---|---|---|---|

| Oil Price (USD) | $61.50 | +18.31% | +26.75% |

| Gold Price (USD) | $1,728.80 | -6.57% | -8.78% |

| US 3 month T-bill | +0.04% | -0.02%* | -0.05%* |

| US 10 year Bond | +1.44% | +0.33%* | +0.51%* |

| USD/CAD FX rate | 1.2685 | -0.74% | -0.37% |

| EUR/CAD FX rate | 1.5348 | -1.06% | -1.67% |

| CBOE Volatility Index (VIX) | 27.95 | -15.53% | +22.86% |

*Absolute change in yield, not the return from holding the security.

February was a strong month for equity markets, much stronger than usual for that month of the year. Fixed income on the other hand, was down almost across the board.

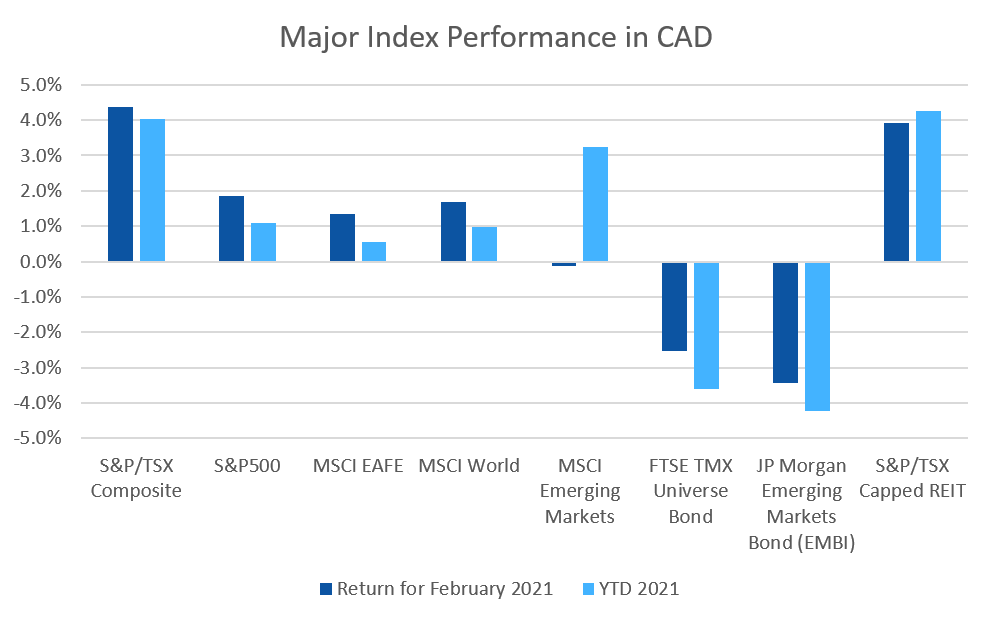

The S&P/TSX Composite was up +4.2%, +3.6% for 2021 so far. The S&P/TSX Small Cap was up more than double that at +9.4% for February. In the US, equity market performance was more subdued; the large cap S&P500 was up +2.8% (+1.7% for 2021) while the small cap Russell 2000 index was up +6.1% for February and +11.5% for 2021.

The broad index of EAFE (Europe, Australasia & Far East) stocks was up +2.5% (+2.1% for 2021), European stocks were up +2.3% and British stocks were up +2.6% for the month. Japanese stocks were another bright spot, up +4.7% for February and +5.5% for 2021 so far. Emerging market stocks were up +1.0% in February and are up +4.7% for 2021.

Bonds were one of the few weak spots in February. The major Canadian bond index, the FTSE/TMX Universe Bond Index, was down -2.5%, its worst month since May 2004. That index is on track for its worst quarterly performance since 1994. The FTSE/TMX Short-term Bond Index was down -0.8%, its worst month since June 2017. US investment grade bonds fared similarly poorly; the ICE BoA AAA and BBB indexes were down -3.3% and -1.8% respectively for February. The AAA index is down -5.5% so far in 2021, its worst drawdown since the 2008-09 financial crisis. High yield did better at +0.3% for HY Master II and +0.6% for the CCC and lower index (the real junky stuff). Emerging market bonds were down -3.4%, their worst month since last March. REITs were up +3.9% in February.

Oil had a very strong February, up +18.3% putting it back above US$60/barrel. Gold gave back -6.6% in February, and is now down -8.8% for 2021. With oil making up a large part of the diversified Bloomberg Commodities Index, it returned +6.5% for February and is +9.3% in 2021, putting it on track for its best year since 2016.

With oil recovering, its taking the Canadian Dollar (CAD) along with it. CAD gained +0.7% against the US Dollar in February, and +1.1% against the Euro.

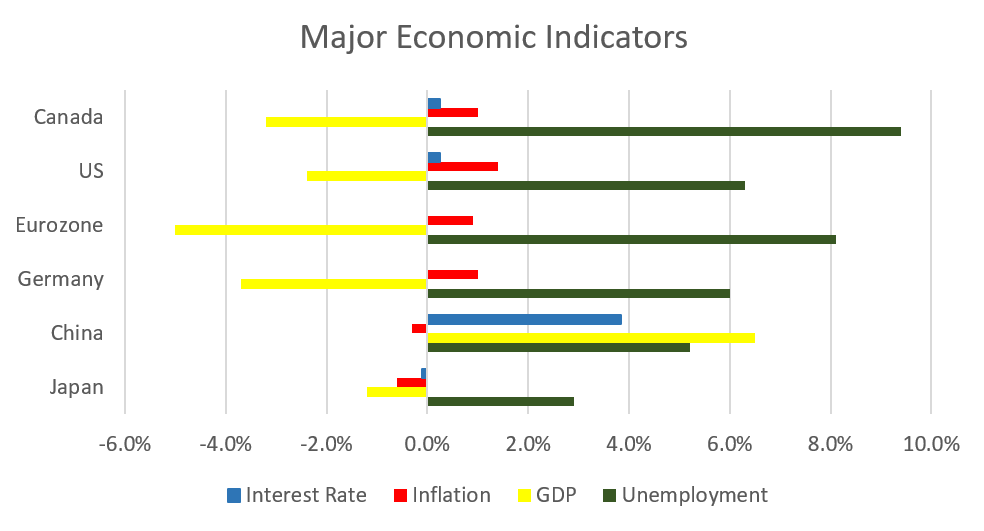

February 2021 Economic Indicator Recap

Below are the readings received in February for the major economic indicators: central bank interest rates, inflation, GDP and unemployment.

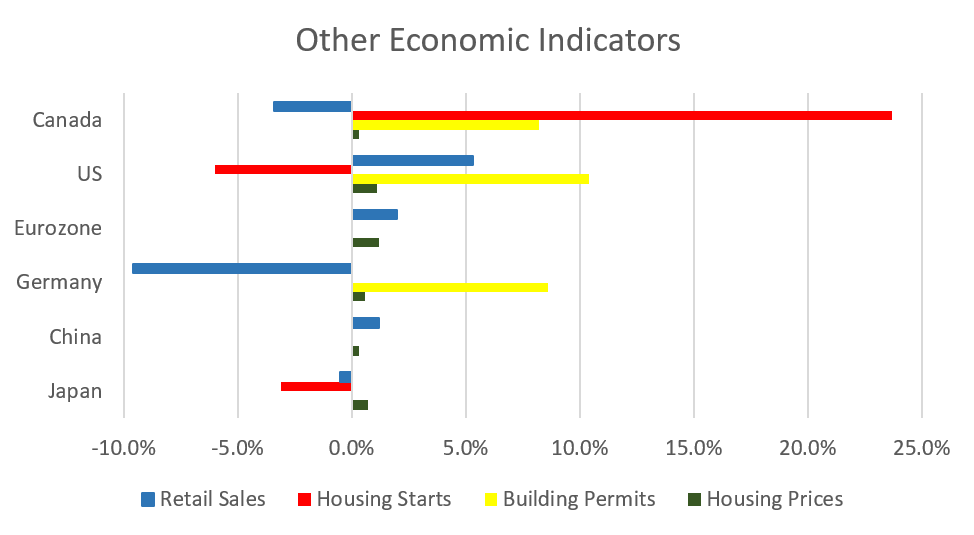

Below are the current readings on a few other often followed economic indicators: retail sales and housing market metrics.

A Closer Look at the Canadian Economy

Canada’s unemployment rate spiked up in January to 9.4%. The economy lost 212,800 jobs during the month, well above the forecasts of a 47,500 decline. 225,400 of the losses were part time jobs which were concentrated in Ontario and Quebec; while full time employment rose 12,600.

Housing prices across Canada were up +0.3% in January. Hamilton was the top performer at +2.0%, followed by Montreal (+1.0%), Victoria (+0.6%) and Halifax (+0.4%), while Toronto, Calgary, Edmonton, and Winnipeg were down for the month.

The level of new housing starts rose a whopping +23.1% in January, with urban construction rising +27.7%. Building permits rose +8.2% to an all-time high $9.9 billion, as residential construction permits rose +10.6% to $7.1 billion.

The inflation rate for January was +0.6%, and +1.0% on an annual basis. Core inflation which excludes more variable items such as gasoline, natural gas, fruit & vegetables and mortgage interest was +1.6%. The cost of transportation, recreation, and food rose.

Retail sales were down -3.4% in December, the first monthly decline since April’s record -24.8% drop. The decline was attributed to increased COVID-19 cases which caused provincial governments to reinstate some social distancing measures. Compared to December 2019 retail sales were up +3.3%. For 2020 overall, retail sales were down -1.4% compared to 2019, the largest annual decline since the 2009 recession.

Canada’s GDP was up +0.1% in December, the eight consecutive monthly gain since the biggest contraction on record in March and April. Collectively the goods producing sectors rose +0.6% while the services sectors declined -0.1%. 12 of 20 industrial sectors posted gains in December. For 2020, 17 of 20 industrial sectors declined; the goods sectors shrank -6.2% in the largest decline since 2009, while the services sectors declined -4.9%, their largest decline since the data series began in 1961.

As expected, the Bank of Canada left its benchmark interest rate at 0.25% at the January 20 meeting. The benchmark interest rate is expected to remain at its current low level until into 2023. The BoC has maintained its quantitative easing program of purchasing at least $4 billion of bonds.

*Sources: MSCI, FTSE, Morningstar Direct, Trading Economics