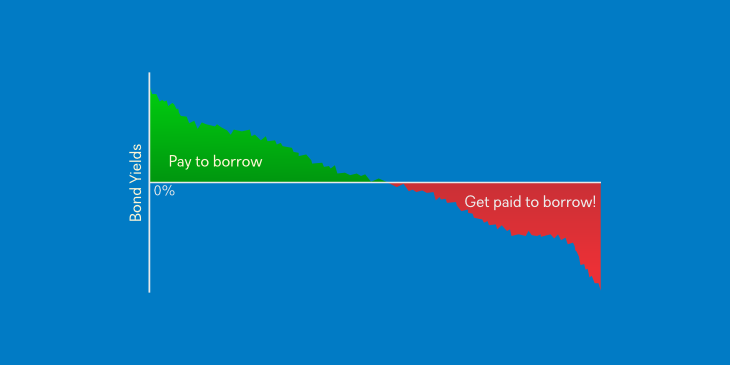

You may think that getting paid to borrow money is impossible, but that is what the Swiss government did recently.As you may have read last week, Switzerland became the first government ever to sell 10 year bonds with a negative yield: on April 7 Switzerland sold 10 year bonds with a yield of -0.055%. How is this possible?

To help explain, let’s review how bonds work.

A bond is an obligation by the borrower to the lender. The borrower agrees to borrow money from the lender for a specified term (the time period of the loan) at a specified interest rate (aka coupon rate). The borrower agrees to pay the lender an interest payment (called a coupon payment) on a set schedule (usually twice per year). At the end of the loan period (aka maturity) the borrower agrees to repay the amount of the loan (called the principal). Bond prices are usually quoted based on a percentage of $100 (known as the face value).

The return on a bond is composed of the interest received and any capital gains or losses. Highly sought after bonds often trade for more than $100, while less sought after bonds trade for less than $100. Less sought after bonds often carry a higher level of risk, but carry the potential for a higher level of return.

If you purchase a bond at $101 and hold it to maturity to receive the $100 principal payment, you will have a capital loss of $1. If you bought a bond for $97 and held it to maturity to receive the $100 principal payment, you have a capital gain of $3. To breakeven on the $101 bond, you would need to receive interest of $1 while you owned it.

| Bond 1 | Bond 2 | |

| Purchase Price | $101 | $97 |

| Maturity Price | $100 | $100 |

| Capital Gain/Loss | -$1 | +$3 |

| Interest Received | $1 | $1 |

| Total Return | $0 | $4 |

A measure called yield to maturity (YTM) takes into account both the coupon payments and the difference between the current price and the maturity value ($100). For simplicity, you can think of this as the total return on the bond.

When a bond is issued, the borrower sets a coupon rate they are comfortable with, perhaps 5%. If this is less than the market rate for comparable bonds, prospective buyers will want a discount to buy the bond and if the coupon rate is higher than the market rate, prospective buyers would be willing to pay a premium. That way the total return on the bond is similar to comparable bonds that are already trading on the market.

That’s a very basic overview of how bonds work. Now let’s apply this to Swiss bonds.

In the case of the latest Swiss government bond sale, prospective buyers were willing to pay a premium for the safety of Swiss debt as Switzerland is one of the few countries with a AAA rating. Australia, Canada, Denmark, Germany, Luxembourg, Norway, Singapore, Sweden and the UK are the others with the top rating from all major bond rating agencies.

The coupon rate on the Swiss 10 year bonds was 1.5%, but since buyers were willing to pay a premium, the yield to maturity was pushed to less than zero (-0.055%).

Other countries in Europe also have debt that currently trade at yields less than 0%: Sweden, Denmark and Germany all have bonds in the 4-10 years to maturity range that trade at a YTM less than 0%.

Most of the headlines claimed that investors were paying the Swiss government, which is technically incorrect. If the coupon rate was negative, the buyer would have to make interest payments to Switzerland, but that is not the case. However, as we discussed above, the buyers are willing to accept a capital loss on their investments.

Why would an investor buy a bond with a negative yield?

In most countries deposits in bank accounts are only insured up to a certain amount ($100,000 in Canada). For that reason, large, institutional investors like banks, pension plans and mutual funds often need to park millions or billions of dollars in cash somewhere other than a bank account at very low risk. It may be that the institutions have an explicit policy to only invest in highly rated securities that they cannot deviate from. It may also be because the investors are willing to accept a small loss to avoid a large loss (like buying insurance). Since there are so many investors in this situation, the demand currently exceeds supply.

Are there other possible explanations for negative bond yields?

Besides a supply/demand imbalance, investors may be expecting deflation to continue such that after taking deflation into account, the real return on the bonds is positive. However, Japan has had periods of deflation for more than a decade, but has only recently had negative bond yields.

Another possible explanation for the negative bond yields is that foreign investors expect that returns on the bonds in their home currency will be positive when translated from Swiss Francs, Euros, Krone, Yen, etc. The implied expectation being that those currencies will continue to appreciate, possibly due to continuing deflation in those countries.

How long can negative yields continue?

Many analysts expect that the yields on Swiss and other high quality bonds will continue to decline as the supply remains low. While the recent Swiss 10 year bond had a coupon rate of 1.5%, Japan’s last 10 year bond was issued with a coupon rate of 0.3%. Coupon rates could potentially reach 0% in many of the countries that currently have negative bond yields.